下载格隆汇APP

下载格隆汇APP

下载诊股宝App

下载诊股宝App

下载汇路演APP

下载汇路演APP

社区

社区

会员

会员

机构:申万宏源

评级:BUY

目标价:24港币

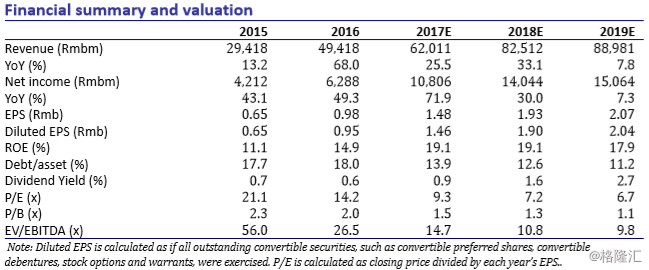

Guangzhou Automobile Group (GAC) reported auto sales of 210k units in January 2018, up 25.1% YoY and 17.9% MoM. We believe the strong sales growth was mainly because domestic high-end products and Japanese brands are gaining traction. We maintain our diluted EPS forecasts of Rmb1.46 in 17E (+53.7% YoY), Rmb1.90 in 18E (+30.1% YoY), and Rmb2.04 in 19E (+7.4% YoY). We maintain our target price of HK$24.00 and, with 48.7% upside, maintain our BUY rating.

Good start. The company realised auto sales of 210k units in January 2018, up 25.1% YoY and 17.9% MoM. Domestic brands recorded total sales of 61k units in January (+32.3% YoY), mainly due to rising demand for high-end Trumpchi products and a healthy days’ sales in inventory, at 0.8 months, by end2017. GAC Honda reported sales of 72k units in January (+38.4% YoY), primarily due to recovering sales of Accord models. GAC Toyota’s January sales were flat at 46k units, however, with Camry’s capacity ramp-up, we expect to see sequential improvement in GAC Toyota’s monthly sales. We believe GAC will benefit from both the growing domestic sports-utility vehicle (SUV) market and increasing sales of Japanese vehicles, and expect the company’s total auto sales to reach 2.3m units in 18E (+13.0% YoY), vs the company’s guidance of 10% YoY growth.

Trumpchi’s improving product mix. We expect GAC to step up development of advanced technologies and products for its domestic brand. We forecast Trumpchi sales of 679k units in 18E (+34.0% YoY) and 725k units in 19E (+6.7% YoY), driven by Trumpchi GS8’s ramping up sales, the launch of the GM8 model, and a mid-life facelift for the GS4. We think GAC will continue to shift its product mix towards higher-end products (GS8, GS7, and GM8), with sales contribution from the three models climbing from 21.8% in 17A to 29.5% in 18E, and blended average selling price rising 1.4% YoY to Rmb92k in 18E. As such, we expect Trumpchi’s blended gross margin to expand from 17.9% in 16A to 22.3% in 17-18E and 22.4% in 19E.

Japanese growth driver. GAC’s JV with Toyota Motor (7203:JP) suffered from tight capacity in 2017, and we expect the capacity issue to be solved in 18E, with 100k units of new capacity commencing operation from the beginning of 2018. We have confidence in two new models based on the Toyota New Global Architecture, Camry, launched in November 2017, and C-HR, to be introduced in mid2018. With strong performance and numerous safety features, the new Camry achieved over 30k orders only two month after its release. We expect Toyota’s sales volume to reach 505k units in 18E (+14.1% YoY) and 528k units in 19E (+4.6% YoY).

Maintain BUY. Given the firm’s improving product mix and margin expansion, we maintain our diluted EPS forecast of Rmb1.46 in 17E (+53.7% YoY), Rmb1.90 in 18E (+30.1% YoY), and Rmb2.04 in 19E (+7.4% YoY). We maintain our target price of HK$24.00 and, with 48.7% upside, our BUY rating.