下载格隆汇APP

下载格隆汇APP

下载诊股宝App

下载诊股宝App

下载汇路演APP

下载汇路演APP

社区

社区

会员

会员

JP Morgan 2016Annual Report

JP摩根2016年报解读

I haven't posted much about JPM recently asit's still basically the same story. Great CEO building an awesome companyperforming really well etc. After even a couple of posts, they are basicallythe same.

最近我没有PO太多关于JP摩根的文章,内容都是大相径庭的,无非是一个伟大的CEO创立了一个优秀的公司,然后就是JP摩根各方面都很优异。我写过几篇关于JP摩根的文章,不过也都是老生常谈。

But since I haven't been too active here recently, I figured why not? Let'stake a look at this. There is a lot to learn here, not just about banking andthe economy, but about markets and investing too.

考虑到我最近不是那么的活跃,我想着为什么不来看一看摩根的年报呢?JP摩根的年报中有很多内容值得学习,不仅仅是关于银行和经济,还有关于市场和投资的内容。

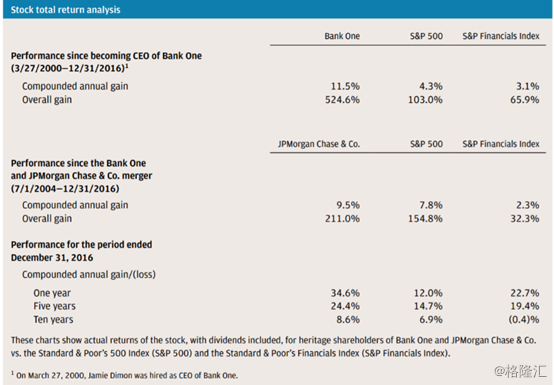

So first of all, let's look at how well JPM has done in recent years. And it'snot just because of the huge bull market since 2008. If you look at theperformance figures below, they go back to 2004, and the performance chart inthe proxy is from 2007, which is the benchmark I use to get 'through-the-cycle'returns.

首先,我们看看JP摩根这几年创造了多少成绩,这些成绩并不只是因为2008年以后迎来来了一波牛市。从下面的业绩数据你可以看到JP摩根的良好经营可以追溯到2004年,不过年报里的业绩表现图是从2007年开始的,我以2007年的数据为基准算出了“周期之后”的投资回报。Check out the total return of JPM stock over various time periods:

各时期JP摩根的股市整体回报情况:

This is really crazy given what hashappened since 2000 and particularly after 2007. Back in 2000, I don't thinkanyone would have guessed JPM stock would outperform the S&P 500 index overthe next 16 years. People were bearish the financials after the collapse of the1999/2000 internet bubble, especially JPM which had a large investment bankattached to it with trillions in notional derivatives outstanding. For years,JPM has been considered the first domino in the coming financial collapse.

2000年后发生的一切真的很疯狂,尤其是2007年之后。2000年的时候,我想不会有人觉得JP摩根的股票在接下来的16年里会超过标准普尔500指数。在1999/2000年互联网泡沫之后,人们对金融市场的预期是看跌的,更不用说JP摩根在该行业进行了大量的投资,发行了数亿元的派生金融产品。许多年来,JP摩根都被认为是在金融风暴中会第一个倒下的多米诺骨牌。

And yet, look at that! Yes, bears willargue that JPM got bailed out during the crisis etc. I've talked about that alot here so won't go into it too much, but I disagree. I agree that thegovernment bailed out the whole system, which is what it should do (that's whatthe Fed is for, and that's what the government has the power to do inextraordinary situations). But I don't think JPM was in any danger unlessthe whole system itself collapsed, in which case nothing would matteranyway.

看看JP摩根的实际表现!当然,那些看跌的人会说JP摩根是在危急关被救了等等之类的。我不同意这样的观点,原因我已经说过太多次,不在这里展开。但是我赞同政府挽救了整个金融市场的说法,当然这也是政府该做的(设立联邦储备的就是干这个的,这也是为什么政府在这样的危机中能拥有如此强大的能力)。我不认为JP摩根当时处于危险之中,除非整个金融系统都垮掉了,不过如果真的垮掉了,那也没什么好说的了。

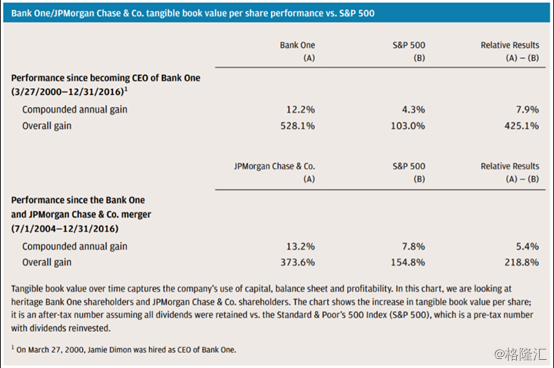

So let's look at the performance of thecompany itself:

现在让我们看看JP摩根的业绩:

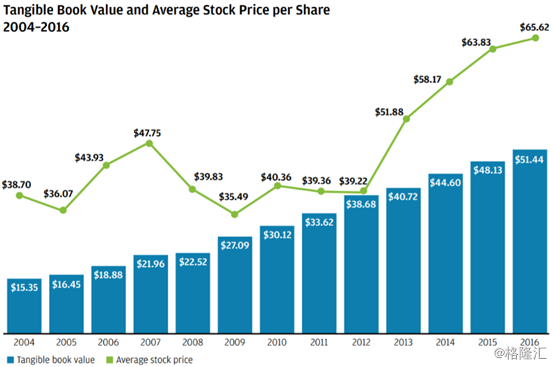

This is just totally insane. TBPS has increased even more than the stock (totalreturn).

这真的是疯掉了,有形资产的账面价值(TBPS)增长甚至超过了股票本身(总回报)Here's a chart from the proxy that is indexed to 2007:

这里年报里以2007数据为基准的JP摩根股票投资回报统计:

That's a 10.5%/year returnsince 2007. That's crazy. Let's say you knew that theworst financial crisis would come and almost destroy the country. People wouldhave called you an idiot if you said, "Fine. I don't care. My stock willreturn 10.5%/year over the next 9 years!". In fact, I did own JPMand didn't sell in front of it, even when cracks appeared. I didn't sell anyduring or immediately after either.

从2007年开始是年10.5%的回报率。在几乎要摧毁整个国家的最糟糕的金融危机当下,能有这样的数据简直是疯狂。如果那时你说,“我不在乎,反正我的股票在接下来的9年都会是10.5%的年回报率。”人们一定觉得你脑子有问题。事实上在这样的情况下,我确实没有抛掉我所持有JP摩根的股票,就算已经出现了一丝崩溃的迹象,我依然没有马上卖掉。

Investment Lessons

投资教训

And here's sort of the lesson on investing. It was widely known that Dimon wasa super-competent manager when he took over Bank One. I think he was alreadyconsidered at the time one of the best managers in finance. When he leftCitigroup, many thought C would collapse because Dimon was the detail guy thatmade sure everything was OK. Sandy was a big picture guy while Dimonchased after the details. No Dimon == noone looking at the details =>eventual blowup. (I heard this from someone that was there at the time andwatched how they worked up close too.)

这儿有一些关于投资的经验教训值得吸取。吉米·戴蒙的超强管理能力人尽皆知,他接管了第一银行,我觉得他当时是金融领域里面最好的经理。他离开花旗集团的时候,很多人觉得花旗集团可能会垮掉,因为戴蒙是一个事无巨细的稳重的管理层。而戴蒙离开之后,喜欢画大饼的桑迪·威尔接手。失去戴蒙=没人掌管一切→最后崩溃。(我是从一个当时还在花旗银行工作的人那儿听到这些的,他很清楚他们是如何紧密合作的)But a lot of people didn't invest in JPM because it was a large money-centerbank and banking cycles tended to be severe. Everyone remembers the bankingcrisis of the 1970's and the late 80's/early 90's.

很多人都没有投资JP摩根,因为它是一个超级大货币中心银行,而且当时周期性的银行业危机已经日趋严重了。70年代和80年代末90年代初的银行业危机是每个人都无法忘记的。

So the thought was 'thanks, but no thanks'. I confess I was one of those.I've owned Bank One since forever and JPM too, but never allowed it to become ahuge position because of that. (On the other hand, I would not mind being 100%in Berkshire Hathaway, even though BRK has gone down 50% on a number of occasions).

所以这个想法就相当于“谢谢你的建议,但是谢谢,我并不需要。”我承认自己曾经也是他们的一份子。我一直都是持有第一银行和JP摩根,但正因为这个原因,我绝对不让JP占太多成投资仓位。(从另一方面来说,就算伯克希尔哈撒韦很多时候跌了50%,我倒是从不在意100%的买伯克希尔·哈撒韦!)

In 2007, bank stocks were expensive and we were at the tail end of a very longcredit cycle. Contrary to the claims of some best-selling books, the leveragebuilt upon shrinking credit spreads was pretty well-known within the industry.It would have been wise to not be too exposed to financials at this point.

2007年,银行股票非常的贵,而且当时处于长期的信贷危机的末尾阶段。跟那些畅销书中说的恰恰相反,在信用贷息差收缩的基础上放高杠杆金融杠杆的做法在业内无人不知。这时候,不暴露在金融股的风险之下是很明智的做法。But, when you own a great business run by great people, it is often better offto ride out the cycles. And that's another lesson here with JPM stock. This isnot really hindsight trading either, as I would have told you back in 2007 thatJPM and GS would be the survivors in any crisis, and they would come out theother end bigger and stronger (as Charlie Munger says about how great companiesgrow; they grow in bad times).

不过,一旦有了杰出的人运营杰出的业务,平安度过周期性的危机就轻松了很多。这是JP摩根带给我们的另外一个教训。这绝对不是放马后炮,早在2007年的时候我就说过JP摩根和高盛可能是金融危机中的幸存者,危机过后它们会发展得更加强大(就像查理芒格说的一样,伟大的企业无论是不是身处好的时代,它都会增长)。The argument back in 2007 really focused a lot on the notional derivativesoutstanding at JPM. This was one of the major red flags that kept someinvestors away. I have managed derivatives before so I understood that notionalamounts outstanding is not a measure of risk. When you are abig banker and dealer, you end up with huge amounts of notionals outstandingbecause, for example, if you issue bonds for an issuer, you sometimes dointerest rate swaps to accommodate the client's cash flow needs. Same with FX.As a major FX dealer, you often use swaps as a tool to help risk-manageclients' risk exposure. Those 'straight' swaps often have very littlerisk.

2007年的时候,大家主要的在意点主要在JP摩根发行的诸多不切实际的金融衍生品上。这是众多危险警报中最亮的一个,它让很多投资者对JP摩根望而却步。我之前管理过金融衍生品,所有我知道发行众多的衍生品并不直接对等风险。如果你是一个大银行家、大额交易员,发行衍生品之后留下的也不过是一大笔衍生品,仅此而已。比如,如果你为发行人发行了债券,很多时候为了迎合客户的现金流需求,你需要做出像做外汇一样进行利率互换。作为一名外汇交易员,你往往会用利率互换为工具来帮助客户控制风险敞口。这种直接交换往往风险很小。

Cyclical or Secular?

周期性还是长期?

The other lesson is that markets have cycles. After the financial crisis andafter JPM has shown its resilience and management competence, it traded cheaplyfor a long time. Even the most prominent bank analysts would say things like,"Yes, it's cheap, but there is no reason to own it as regulations make ithard for them to make money...". I've heard that argument over and overagain post-crisis.

另外一个经验就是:市场是周期性的。金融危机之后,JP摩根展示出了自己的复原力以及管理能力,在很长一段时间内它的交易价格都很便宜。不过,就算是业内最优秀的银行业研究员说出来的话都是:“是的,它(JP摩根)很便宜,但是在危机后出台的法规下, JP摩根想盈利实在是太难了… ”。金融危机之后,我不止一次听到过这番言论。

But these folks held a linear, static model in their heads. They didn'trealize, or underestimated how the industry would adjust to new regulations andrequirements. If the regulatory capital burden got too heavy in a line ofbusiness, they would drop it. They can cut expenses. They can reprice productsas new regulations apply across the industry.

但是这些人的想法太一根筋,太一尘不变了。他们没有意识到整个行业会自我调整适应新的法规和要求。如果整个行业里资本监管的担子过重,金融机构可以直接放弃掉某些产品项目,他们可以节省开支,或者在行业下发了新法规时给产品重新定价。

Maybe this was due to the short-term nature of Wall Street; with regulatoryheadwinds and low interest rates, bank stocks were simply not recommendable.

可能是由于华尔街有注重短期的习惯,一旦法规上出现顶头风、利率又低,银行股就直接被打入不推荐的行列里了。

Either way, long term value investors look to invest in great businesses atreasonable (or cheap if available) prices.

无论如何,长期的价值投资者希望追求的是以合理的价格(或者便宜的价格)买入伟大企业的机会。

And interestingly, now, hedge funds and others seem to bepiling into banks. Nobody wanted JPM at $20 or even $40, and now they arepiling in at over $80! And people say the market is efficient, pickedover etc.

有趣的是,现在很多对冲基金,还有一些投资者好像都蜂拥着去投资银行股。当初JP摩根卖20美金,40美金的时候没人买,现在到80美金了却有一大批人冲去买!现在大家就开始说起市场是有效的,经过了筛选的,诸如此类的话。

I think all of this sort of just illustrates the cyclical nature of markets.The key in successful investing is being able to see the difference betweencyclical and secular. It's true that this is very hard a lot of the time. But Inever thought banking itself was in secular decline. Every year, Dimon hasshown how much business needed to be done over the long term in banking.

我觉得这一切都表明了市场是周期性的。取得投资上的成功关键在于区分开周期性和长期性。诚然,这自始至终都特别难。但是我从不认为银行业本身是出于长期性衰落的阶段。每一年,戴蒙都表示从长期来看银行业还有大量的工作业务要完成。

Regulations tend to be cyclical too as the pendulum can swing wildly from oneextreme to the other. We are now seeing the pendulum start to swing back theother way. As Dimon says, a lot of this can be done (simplify regulations)without congressional action.

法规也有周期性倾向,因为政治主张也会从一个极端摇摆到另一个极端。我们现在正在经历政治主张摇摆到另外一方的过程。正如戴蒙所言,只要没有国会插手,很多事情都是能办到的(简化法规)。

I do believe that this max exodus out of hedge funds too is cyclical, as is themove towards machines (vs. people) / indexing. I do believe that most hedgefunds probably don't deserve to exist, and machines will more and more takeover money management, but I think it will still be very cyclical. Wehave seen this before in the past; move to quantitative money management,indexing vs. active, hedge funds vs. index etc...

我相信现在大批量不看好对冲基金的行为也是有周期性的,像现在很多人投向机器投资,或者指数基金一样。的确,我绝对额很多对冲基金或许没有存在价值,机器也可能会逐渐抢走资产管理的工作,但是我觉得周期性还是存在的。过去我们经历过类似的事情;一开始是走向量化资产管理,投资指数,然后是积极投资,对冲基金,现在指数型投资又回来了,等等…。

Buffett and WFC

巴菲特和富国银行

And this sort of thing explains why Buffett has been buying WFC for all theseyears, even right before the crisis. I always heard comments like, "doesn'tBuffett see this big trouble brewing? This huge storm? Doesn't heunderstand that the era of big banks is over?". He has been buying before,during and after the crisis at 'high' prices.

这部分我主要想说说巴菲特为何在金融危机当前依然买入了富国银行并一直持有。我经常听到这样的评论,“巴菲特难道没有看到一场金融危机正在酝酿中吗?他难道没有预见暴风雨即将到来?他难道没看到银行的时代已经结束了么?” 其实巴菲特在危机前、中、后期都“高价”买入过富国银行。

He focuses on what a business can earn on a normalized basis over time, so hedoesn't care about the short term outlook. He doesn't care about what otherpeople say. He doesn't worry about downturns as strong institutions should bemanaged to survive and grow in such situations. Trading in and out to avoidsuch dips is a loser's game.

巴菲特看重的是一个企业长期的常规性盈利能力,所以短期的经营状况对他来说并不重要。他也不在意别人是什么看法。他不会为下行走势担心,因为强大的企业在这样的情况下应当具备复苏和增长的能力。为了避免这样的下行而买入卖出显然是输家的游戏。

2004年到2016年富国银行有形资产帐面价值及平均每股股价2x Tangible Book

2倍有形资产账面价值

Dimon says it was a no-brainer to buy back stock at 1x tangible book, but saysthis year that it still makes sense to buy back stock at 2x TBPS. That would beover $100/share!

戴蒙曾经说过,当股票价格是有形资产账面价值的一倍时可以无脑回购股票,照现在这些年的情况来看,按照2倍有形资产账面价值(TBPS)回购股票也是行得通的。这样来看那就是100多美金一股!

That sounds insane. Who would have evenguessed JPM would be closing in on $100 just a couple of year ago?

听起来太疯狂了。几年前谁能预料到JP摩根将来会以100美金收盘呢?

Assuming a 50% payout ratio on $6.00 or soin EPS, that would be $3.00/share in dividends. Usinga $100/share price, that's a 3% dividendyield. Assuming JPM grows along with the economy (4% nominal), that's anexpected total return of 7%/year against what I would assume anormalized long term rate of 4% (actual is 2.3%). As a sanity check, EPSgrew around 4%/year from 2007 to 2016.

假设EPS6美金的派息率是50%,那么股息是3美金一股。假设 JP摩根的增长跟整体经济增长水平保持一致(通常是4%),那么每年的总体回报率是7%,我给出的长期平均回报率是4%(实际上是2.3%)。再核对一下,EPS从2007年到2016年每年增长4%。

OK, students will immediately jump on meand argue that earnings growth should be 6.5%/year for a 9.5%/year return(50% retention at 13%). Well, JPM is a big bank so it may not be able to growthat much more than GDP over time, so let's just say earnings grow at nominalGDP. That would just mean that payouts would be higher as capital can'tbe invested at a 6.5% growth rate.

OK,学生这时候会马上跳起来说盈利增长应该是6.5%每年,回报率应该是9.5%每年(50%保留13%)。不过,JP摩根规模很大,所以长期来看它的增长不会超过GDP,所以我们按照常规CDP的增长率算作JP摩根的盈利增长。这也就意味着派息率会高一些,因为资金无法投资到6.5%的增长率上。

In that case, payouts may be 70%. Ona $6/share EPS, a 70% payout is a $4.20/share dividend for ayield of 4.2% (again, at a $100 stock price). 4.2%dividend yield plus 4% growth is 8.2% expected return.

在这种情况下,派息率可能达到70%。如果EPS是6美金,70%的派息率意味着拍戏4.2美金,这样回报率是4.2%(同样,按照每股100美金来算)。4.2%加上4%的增长,那么预期收益率就是8.2%。

Of course, as we wait for things tonormalize, bad debt may normalize too; JPM is sort of over-earning in the sensethat credit trends are really good now. This has probably bottomed out andshould head higher. I don't think there are any time bombs at JPM, but it willsort of be a race on the economy picking up steam and interest ratesnormalizing versus credit trends bottoming out.

当然,在我们等候事情常规化的过程中,坏账可能也常见起来;目前信用趋势向好,从这个层面来说JP摩根实现了超额盈利。这可能是信用水平刚刚走出最低点,应该会继续往上走。我觉得JP摩根不存在潜在的炸弹,但这肯定是一场经济逐渐好转、利率回归正常水平跟信用趋势走好之间的较量。

Cheap Labor

廉价劳动力

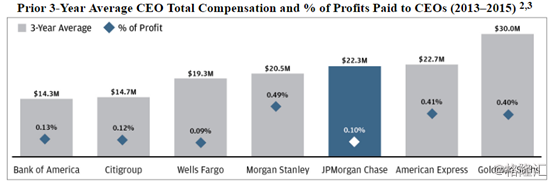

The great thing about JPM is that we get all of this for so cheap. We paidDimon 0.1% of profits. Compare that to other financials! Let'snot get into hedge fund fees here.

JP摩根很好的一点在于它的劳动力成本很低,戴蒙的薪资是公司利润的0.1%,跟其它的金融机构以对比就可以看出差距!这里我们不考虑对冲基金的费用。

注:美国各大金融机构CEO薪资水平,及其占机构净利润的比重。

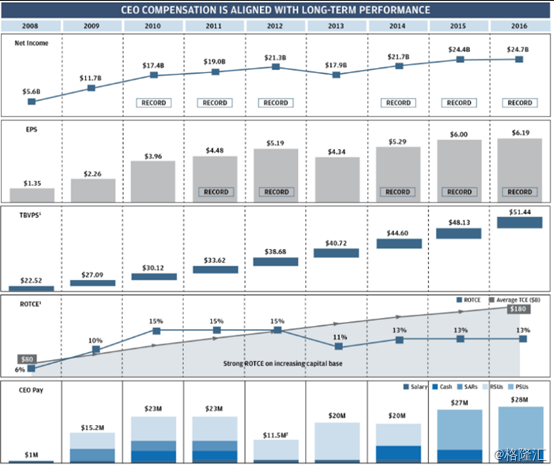

注:CEO薪酬与企业长期表现匹配图